Zapmap and the Green Finance Institute (GFI) have published the third edition of their utilisation report, assessing how the public network has responded to the 470,000+ increase in EV drivers across 2025, and providing an updated view of whether the demand from EV drivers has outpaced the increase in supply of public EV chargers.

Covering Q1 2024 to Q4 2025, the report compares observed power delivery against stated capacity and is designed to equip investors, policymakers, and charge point operators with a clearer understanding of how utilisation, efficiency, and on-site energy management will define the next phase of the UK’s EV charging rollout.

Utilisation rates remain stable despite material capacity growth

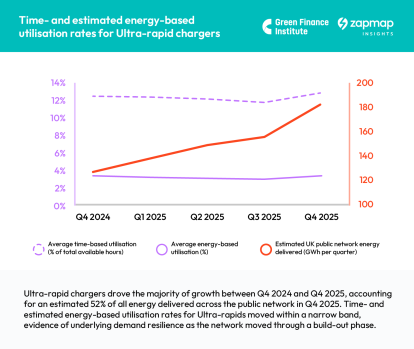

Ultra-rapid chargers drive majority of energy delivered across the public network

Key findings from the report:

The public charging network is still growing steadily, with more new EV chargers being built at higher power levels

As of December 2025, the UK had 116,052 publicly available EV chargers, up 13% year-on-year (+13,281). The number of Ultra-rapid EV chargers of 150kW and above grew by 40% reflecting accelerated rollout of high-powered assets, while around half of all public chargers fall within the Standard band (3-7.9kW), typically used for long stay or overnight charging.

Average utilisation remained broadly stable despite material capacity growth

Time- and estimated energy-based utilisation rates moved within a narrow band across all power categories, even as the public charging network grew 13% and total energy delivered grew an estimated 21%, evidence of underlying demand resilience as the network moved through a build-out phase.

Total estimated energy delivered grew 21% between Q4 2024 (289 GWh) and Q4 2025 (350 GWh)

Ultra-rapid chargers drove the majority of this growth, accounting for an estimated 52% of all energy delivered across the public network in Q4 2025, up from 44% a year earlier.

Ultra-rapid utilisation has held up despite a 40% expansion of the asset base

Due to their high energy demands, typically charging hubs incorporating multiple Ultra-rapid EV chargers present the greatest potential challenges for grid resilience. Time-based utilisation of Ultra-rapid (150kW+) EV chargers averaged 12.8% in Q4 2025, broadly in line with Q4 2024 (12.4%) and Q1 2024 (12.4%), a notable result given the band grew by 3,425 chargers (+40%) over the year.

EV chargers often deliver less power than their stated maximum rating

Ultra-rapid chargers exhibit the largest gap between stated capability and observed transfer rates, at an average of 55.4kW, representing roughly 26% of their stated rating. This is largely driven by vehicle acceptance limits, charging curves, and grid constraints.

Leading operators are improving performance while managing grid capacity costs

They are deploying dynamic load balancing, modular power architectures, and on-site battery storage to improve throughput consistency and reduce the cost of capacity.

This year, Zapmap and the Green Finance Institute have also incorporated first-hand insights from charge point operators and an iDNO to provide real-world, evidence-based examples of how leading stakeholders are moving beyond initial installation to focus on operational efficiency and grid-smart infrastructure to ensure that EV drivers arriving to charge at a site are able to access the highest power transfer possible for their vehicle.

Together, the case studies showcase strategies being deployed to translate installed capacity into reliable, revenue-generating throughput:

- Osprey Charging Network: utilising dynamic load balancing and proprietary software to allocate power in real-time, preventing capacity from being "locked" in unused bays.

- Moto Hospitality: investing in site design and on-site solar energy to generate capacity beyond the grid and support high-throughput destinations.

- Eclipse Power: employing phased capacity and "capacity banking" to secure grid connections early while activation occurs in stages to manage costs.

Jade Edwards, Head of Insights at Zapmap, commented:

"The fact that utilisation has held steady despite a 40% expansion in Ultra-rapid infrastructure is a powerful indicator that the UK's charging network is not just growing, but is also becoming increasingly resilient.

"What is particularly encouraging in this latest report is seeing how leading operators are already bridging the gap between rated and real-world power. By deploying dynamic load balancing and on-site storage, the industry is making the network more resilient and efficient, measures that are vital for building driver confidence. Knowing that a site can manage peak demand intelligently ensures that the next wave of EV adopters will find a reliable and capable public network ready for them."

Jonathan Heybrock, Green Finance Institute, commented:

"As the UK’s drivers increasingly adopt EVs, it is vital that we equip investors, policymakers and charge point operators with a clearer understanding of how utilisation and efficiency will define the next phase of the EV rollout.

"This third edition of the paper highlights the 'efficiency gap' between kW stated power ratings and real-world delivery, a factor that is now central to financial modelling for those funding the decarbonisation of road transport. By showcasing how site hosts and operators use phased capacity, battery buffering and on-site energy storage, we aim to demonstrate that the business case for these sites remains strong and is effectively future-proofed for the next generation of vehicles."

For this edition of the report, utilisation is calculated at EV charger level rather than at device level, reflecting a 2026 industry shift in how the UK charging network is counted. The analysis covers live data feeds and observed sessions from Q1 2024 to Q4 2025.

The full report, GFI Utilisation Paper: Edition 3 (2026), can be downloaded here.